Most business owners think the funding process ends once they’re approved.

In reality, that’s when the real evaluation begins.

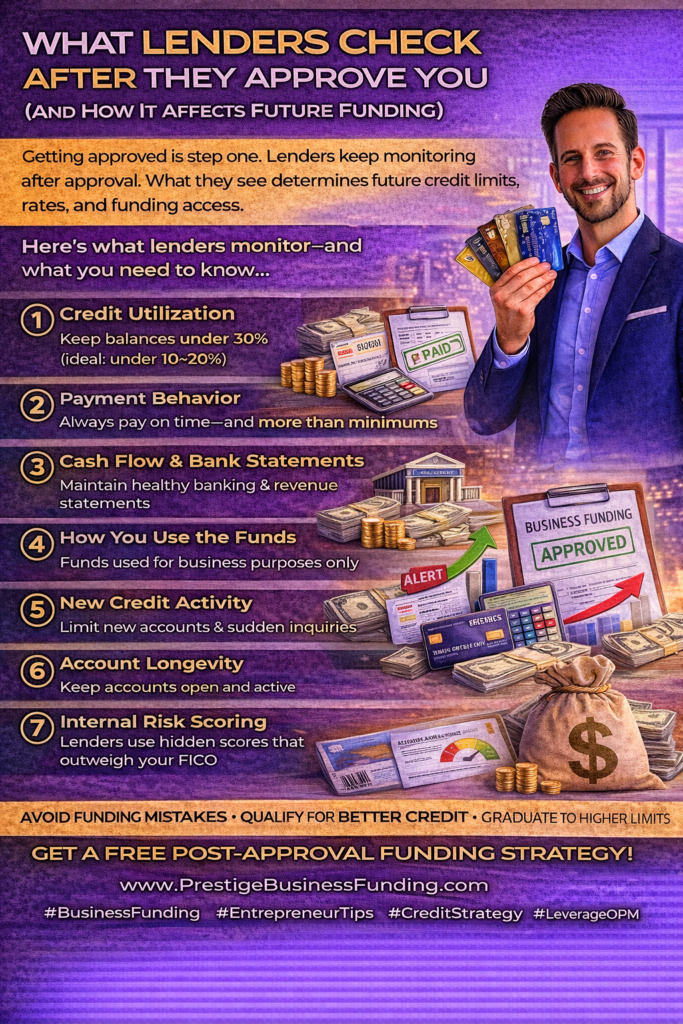

In 2025, lenders don’t just approve and forget. They continue monitoring borrowers after approval, and what they see determines whether you’ll qualify for larger limits, better terms, or future funding—or quietly get cut off.

This article explains what lenders check after approval, why it matters, and how smart entrepreneurs use this phase to unlock even more capital.

Why Post-Approval Behavior Matters More Than You Think

Approval is only step one.

Lenders want to answer a bigger question:

“Did we make the right decision lending to this borrower?”

Your behavior after approval tells them:

- How risky you really are

- Whether you deserve higher limits

- If you qualify for repeat funding

This data shapes your long-term funding power.

What Lenders Monitor After You’re Approved

1️⃣ Credit Utilization (Immediately)

One of the first things lenders watch is how fast and how much you use the credit.

Red flags:

- Maxing out accounts quickly

- Carrying high balances month after month

Best practice:

- Keep utilization below 30%

- Ideal for future funding: under 10–20%

High utilization signals desperation, not strategy.

2️⃣ Payment Behavior

On-time payments aren’t optional—they’re expected.

What lenders track:

- Payment timing

- Consistency

- Minimum vs. larger payments

Late payments or minimum-only patterns reduce trust and future approval odds.

3️⃣ Cash Flow & Bank Statements

For business funding, lenders often review:

- Average daily balance

- Deposit consistency

- NSF or overdraft activity

Clean banking behavior increases funding confidence—even without perfect credit.

4️⃣ How You Use the Funds

Yes, lenders can infer usage.

They look for signs that funds are used for:

✔ Business expenses

✔ Revenue-producing activities

✔ Growth or stabilization

Using business credit for personal spending is a silent funding killer.

5️⃣ New Credit Activity

After approval, lenders watch:

- New inquiries

- Additional accounts opened

- Credit stacking behavior

Opening too much credit too fast can trigger internal risk alerts—even if your score stays high.

6️⃣ Account Longevity

Keeping accounts open and active matters.

Closing accounts early or paying them off too fast can:

- Reduce internal trust

- Limit future limit increases

Responsible, steady usage builds a positive funding history.

7️⃣ Internal Risk Scoring

Many lenders use internal scores you never see.

These scores factor in:

- Behavior patterns

- Utilization trends

- Payment consistency

- Overall exposure

These internal scores often matter more than your FICO.

How Post-Approval Behavior Affects Future Funding

What you do after approval determines:

- Credit limit increases

- Access to higher-tier products

- Pre-approved offers

- Lower interest rates

- Repeat funding approvals

Bad behavior quietly closes doors.

Good behavior opens bigger ones.

How Smart Business Owners Use This to Their Advantage

1️⃣ They Treat Early Funding as a Test Run

Experienced entrepreneurs know:

- The first approval is a trial

- Lenders are watching closely

They focus on proving reliability—not maximizing usage.

2️⃣ They Maintain Low Utilization on Purpose

Even when credit is available, they:

- Use only what’s needed

- Keep balances controlled

- Pay down strategically

This signals strength and discipline.

3️⃣ They Time Future Applications Carefully

Instead of rushing, they:

- Let accounts age

- Improve post-approval metrics

- Apply when their profile is strongest

Timing alone can double approval amounts.

4️⃣ They Build Business Credit Alongside Personal Credit

This reduces dependence on personal credit and:

- Improves approval terms

- Unlocks EIN-based funding

- Lowers personal risk over time

Common Mistakes That Hurt Future Funding

Avoid these post-approval errors:

❌ Maxing out accounts immediately

❌ Missing or late payments

❌ Opening multiple accounts too fast

❌ Mixing personal and business expenses

❌ Ignoring bank statement health

These mistakes don’t always cause instant denial—but they limit growth.

Why This Matters More in 2025

With tighter lending standards, lenders prefer:

- Fewer borrowers

- Stronger behavior

- Proven reliability

Post-approval behavior is now one of the strongest predictors of future funding access.

Final Thoughts

Getting approved is only the beginning.

What you do after approval determines whether you:

- Stay stuck at small limits

- Or unlock $50K–$250K+ in future funding

Smart entrepreneurs don’t just get approved—they graduate to better funding.

Need Personal Or Business Funding? Prestige Business Financial Services LLC offer over 30 Personal and Business Funding options to include good and bad credit options. Get Personal Loans up to $100K or 0% Business Lines of Credit Up To $250K. Also Enhanced Credit Repair ($249 Per Month) and Passive income programs (Can Make 5-10% Per Month; Trade $100K of Someone Esles Money). Our 2nd Passive Income Program could make 1-2% Per Day Compounding ($500 to Start, In 2 years could be $6 Million).

Book A Free Consult And We Can Help – https://prestigebusinessfinancialservices.com

Email – anthony@prestigebfs.com

Phone- 1-800-622-0453

🚀 Call to Action

If you want to:

- Use approved credit strategically

- Increase limits and access more funding

- Avoid silent funding mistakes

- Build long-term funding power

Prestige Business Financial Services can help you create a post-approval strategy that lenders reward.

👉 Visit: www.prestigebusinessfinancialservices.com

👉 Or message “Funding Strategy” for a free credit & funding evaluation