Most small business owners believe fixing credit takes years of waiting, disputing, and hoping.

That belief alone keeps thousands of entrepreneurs locked out of funding every year.

Here’s the truth lenders don’t explain clearly:

👉 Credit repair doesn’t have to take years — if you know what actually moves the needle for funding.

In 2025, the fastest credit improvements come from strategic credit optimization, not slow, outdated methods. This guide explains how business owners fix credit efficiently, avoid common traps, and position themselves for funding much faster than most people realize.

Why Traditional Credit Repair Feels So Slow

Most people approach credit repair the wrong way.

Common slow methods include:

- Disputing everything at once

- Waiting on credit bureaus month after month

- Ignoring utilization and structure

- Focusing only on score, not fundability

These approaches may help eventually — but they don’t help when funding is the goal.

What “Fast Credit Repair” Really Means

Fast credit repair doesn’t mean shortcuts or illegal tactics.

It means:

- Fixing high-impact items first

- Improving lender-visible risk factors

- Optimizing how credit is used, not just what’s reported

- Positioning credit for approvals, not perfection

📌 The goal isn’t a perfect score — it’s a fundable profile.

The #1 Reason Business Owners Get Stuck

Many business owners ask:

“Why is my score decent, but I still can’t get approved?”

Because lenders don’t approve scores — they approve patterns.

They look at:

- Utilization trends

- Recent behavior (last 30–90 days)

- Inquiry velocity

- Account structure

- Payment consistency

Fixing these areas creates fast results.

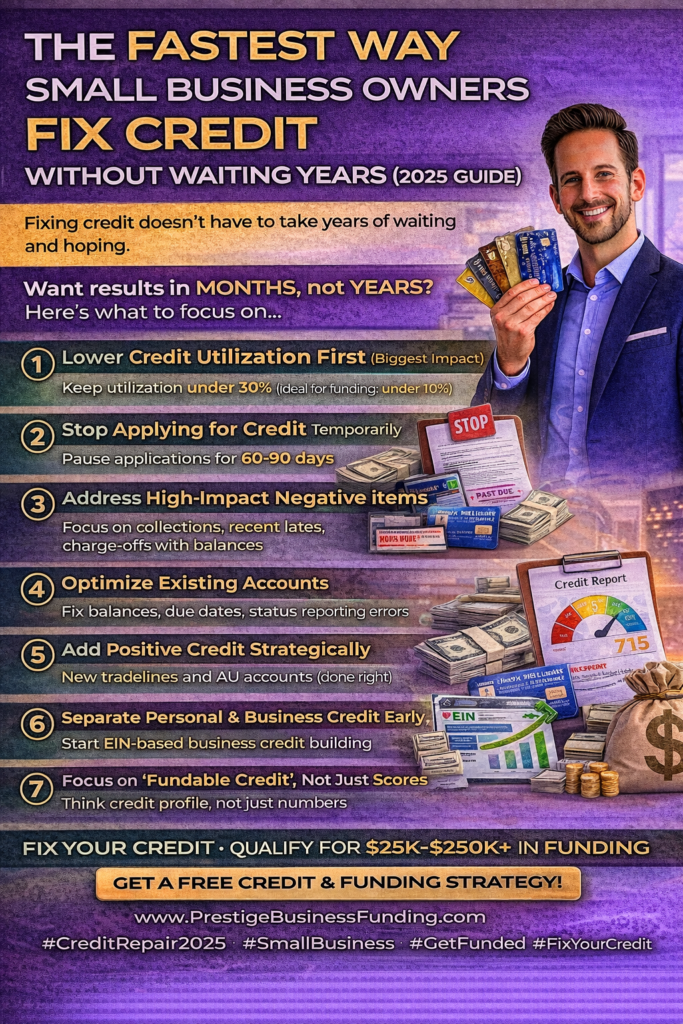

✅ The Fastest Way Small Business Owners Fix Credit

1️⃣ Lower Credit Utilization First (Biggest Impact)

Nothing boosts credit faster than utilization.

Best practice in 2025:

- Keep utilization below 30%

- Ideal for funding: under 10%

Even without deleting a single negative item, lowering balances can increase scores in 30–45 days.

2️⃣ Stop Applying for Credit Temporarily

Each new inquiry signals risk.

Fast fix:

- Pause applications for 60–90 days

- Let recent inquiries age

- Allow credit to stabilize

This alone improves approval odds dramatically.

3️⃣ Address High-Impact Negative Items

Not all negatives matter equally.

Focus first on:

- Collections with balances

- Recent late payments

- Charge-offs reporting balances

Removing or settling the right items produces faster results than disputing everything.

4️⃣ Optimize Existing Accounts (Not Just Remove Bad Ones)

Many people overlook this.

Fast optimizations include:

- Adjusting due dates

- Ensuring accounts report correctly

- Fixing inaccurate balances

- Removing outdated remarks

Small corrections can produce meaningful score jumps.

5️⃣ Add Positive Credit Strategically

Credit improves fastest when positive data outweighs negative data.

This may include:

- Authorized user accounts (done correctly)

- New revolving accounts with low balances

- Properly reported business tradelines

📌 The key is timing and structure, not volume.

6️⃣ Separate Personal and Business Credit Early

Small business owners get stuck when everything runs through personal credit.

Fast-track strategy:

- Establish business credit reporting

- Use EIN-based tradelines

- Build business credit alongside personal repair

This reduces pressure on personal credit and expands funding options.

7️⃣ Focus on “Fundable Credit,” Not Just Scores

This is the biggest mindset shift.

Fundable credit means:

- Clean recent history

- Low utilization

- Minimal inquiries

- Strong payment behavior

Many owners qualify for funding with mid-600 scores once their profile is optimized.

How Fast Can Results Really Happen?

When done correctly:

- 30–45 days: utilization improvements

- 60–90 days: profile stabilization

- 90–120 days: significantly better funding outcomes

Most delays happen because people fix the wrong things first.

Mistakes That Slow Credit Repair Down

Avoid these common traps:

❌ Disputing everything at once

❌ Opening too many accounts

❌ Chasing a “perfect” score

❌ Ignoring business credit

❌ Applying for funding too early

Each mistake adds months — sometimes years — to the process.

Why Credit Repair and Funding Must Work Together

Credit repair without a funding strategy leads to frustration.

Funding without credit preparation leads to denials.

The fastest results come when:

✔ Credit repair is goal-driven

✔ Funding requirements guide the process

✔ Timing is planned, not rushed

That’s how business owners move faster than the average consumer.

Final Thoughts

Fixing credit doesn’t have to take years — but it does require strategy.

When small business owners:

- Focus on high-impact actions

- Optimize behavior lenders actually see

- Build business credit alongside personal repair

They unlock funding opportunities much sooner than they ever expected.

Need Personal Or Business Funding? Prestige Business Financial Services LLC offer over 30 Personal and Business Funding options to include good and bad credit options. Get Personal Loans up to $100K or 0% Business Lines of Credit Up To $250K. Also Enhanced Credit Repair ($249 Per Month) and Passive income programs (Can Make 5-10% Per Month; Trade $100K of Someone Esles Money). Our 2nd Passive Income Program could make 1-2% Per Day Compounding ($500 to Start, In 2 years could be $6 Million).

Book A Free Consult And We Can Help – https://prestigebusinessfinancialservices.com

Email – anthony@prestigebfs.com

Phone- 1-800-622-0453

🚀 Call to Action

If you want to:

- Fix credit the right way

- Avoid wasting months on low-impact actions

- Position yourself for personal or business funding

- Qualify for $25K–$250K+ in funding faster

Prestige Business Financial Services can help you build a custom credit and funding strategy.

👉 Visit: www.prestigebusinessfinancialservices.com

👉 Or message “Fast Credit Fix” for a free credit & funding evaluation