Most business owners believe lenders focus mainly on credit scores.

In reality, your business bank statements often carry MORE weight than your credit report—especially in 2025.

👉 Lenders use your bank statements to answer one critical question:

“Can this business manage money responsibly?”

This guide reveals what lenders really look for inside your bank statements, the hidden red flags that silently kill approvals, and how to fix them before you apply for funding.

Why Business Bank Statements Matter More Than Ever

In 2025, lenders use automated underwriting systems that analyze banking behavior just as closely as credit.

Your statements tell lenders:

- How you manage cash flow

- Whether your income is stable

- If your business is financially disciplined

- How risky lending to you would be

Even borrowers with good credit get denied because of banking red flags.

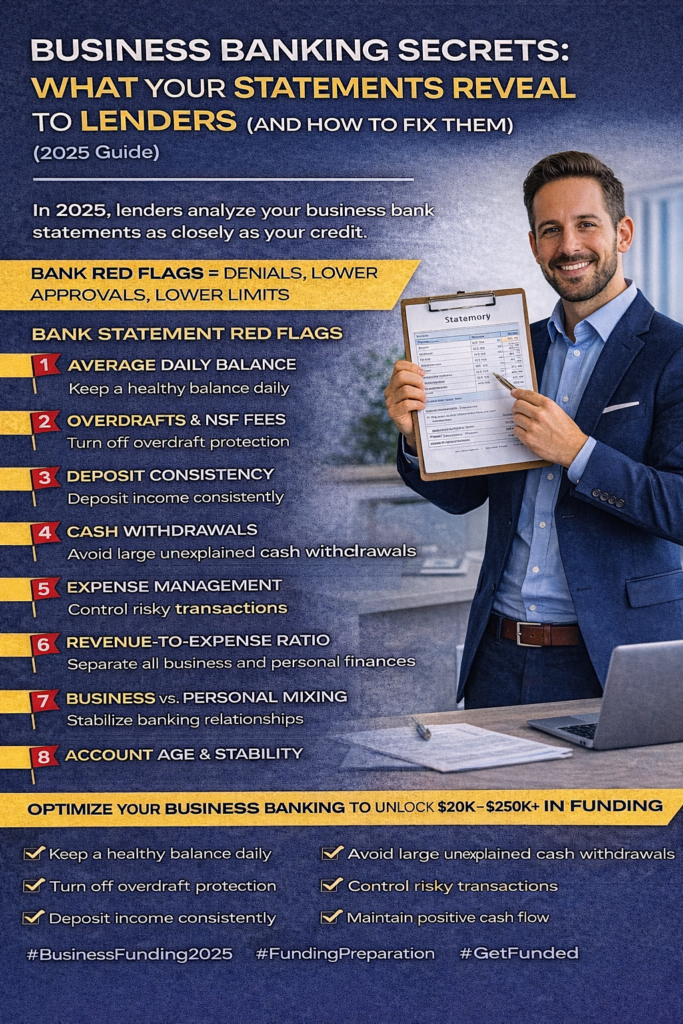

🔍 What Lenders See When They Review Your Bank Statements

1️⃣ Average Daily Balance (ADB)

This is one of the most important metrics lenders analyze.

What lenders want to see:

- Consistent balances

- Enough cash to cover expenses

- No frequent drops to near zero

Why it matters:

Low average balances signal financial stress—even if deposits are strong.

How to fix it:

- Keep a minimum cushion in your account

- Avoid draining the account between deposits

- Delay large withdrawals during funding prep

2️⃣ Overdrafts & NSF Fees

This is a major red flag.

Even one overdraft in the last 60–90 days can:

- Reduce approval amounts

- Trigger higher interest rates

- Cause automatic denials

How to fix it:

- Turn off overdraft protection

- Monitor balances daily

- Keep buffer funds in the account

3️⃣ Deposit Consistency

Lenders prefer predictable income over spikes.

Red flags include:

- Inconsistent deposits

- Large unexplained gaps

- Heavy reliance on cash deposits

How to fix it:

- Deposit income regularly

- Avoid lump-sum cash deposits

- Document unusual income

4️⃣ Cash Withdrawals

Frequent or large cash withdrawals raise concerns.

Lenders may assume:

- Poor bookkeeping

- Untracked spending

- Higher risk activity

How to fix it:

- Reduce cash withdrawals

- Use debit or ACH transactions

- Keep clear records

5️⃣ Expense Management

Lenders analyze how money leaves your account.

They look for:

- Recurring expenses

- Controlled spending

- Minimal gambling, crypto, or high-risk transactions

How to fix it:

- Avoid risky transactions before applying

- Clean up unnecessary subscriptions

- Keep expenses business-related

6️⃣ Revenue-to-Expense Ratio

Strong revenue doesn’t matter if expenses are out of control.

Lenders want to see:

- Income exceeding expenses

- Positive monthly cash flow

- Manageable obligations

How to fix it:

- Reduce unnecessary spending

- Improve margins

- Delay non-essential purchases

7️⃣ Business vs. Personal Separation

Mixing finances is one of the fastest ways to get denied.

Red flags include:

- Personal expenses in business accounts

- Transfers without explanation

- Shared accounts

How to fix it:

- Separate business and personal banking

- Pay yourself a consistent owner draw

- Maintain clean bookkeeping

8️⃣ Account Age & Stability

New or frequently changed accounts raise concerns.

Lenders prefer:

- Established business accounts

- Stable banking relationships

- No frequent bank switching

How to fix it:

- Keep one primary business account

- Avoid opening new accounts during funding prep

What a Funding-Ready Bank Statement Looks Like

Businesses that get approved consistently show:

- No overdrafts or NSF fees

- Consistent deposits

- Healthy average daily balances

- Clean expense patterns

- Clear business income

- Stable cash flow trends

This profile dramatically increases approval odds and funding limits.

When to Fix Your Banking Before Applying

The ideal preparation window is 60–90 days before applying.

This allows:

✔ Negative activity to age

✔ Positive trends to report

✔ Lenders to see stability

Rushing applications without fixing banking issues can cost $25K–$100K+ in lost funding.

Final Thoughts

Most funding denials aren’t caused by bad credit — they’re caused by bad banking habits lenders never explain.

Once your bank statements reflect:

- Stability

- Discipline

- Predictability

Funding becomes easier, cheaper, and repeatable.

Need Personal Or Business Funding? Prestige Business Financial Services LLC offer over 30 Personal and Business Funding options to include good and bad credit options. Get Personal Loans up to $100K or 0% Business Lines of Credit Up To $250K. Also Enhanced Credit Repair ($249 Per Month) and Passive income programs (Can Make 5-10% Per Month; Trade $100K of Someone Esles Money). Our 2nd Passive Income Program could make 1-2% Per Day Compounding ($500 to Start, In 2 years could be $6 Million).

Book A Free Consult And We Can Help – https://prestigebusinessfinancialservices.com

Email – anthony@prestigebfs.com

Phone- 1-800-622-0453

🚀 Call to Action

If you want help:

- Reviewing your bank statements like a lender

- Fixing red flags before you apply

- Structuring your business for funding

- Qualifying for $20K–$250K+ in business funding

Prestige Business Financial Services can help.

👉 Visit: www.prestigebusinessfinancialservices.com

👉 Or message “Banking Review” for a free funding evaluation